LODR Amendments: revised RPT framework and SEBI’s Digital Push

by Supreme Waskar (Partner) and Dipesh Nassa (Trainee Associate)

Introduction

On November 18, 2025, Securities Exchange Board of India (“SEBI”) notified several important amendments to Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015. Many of these key changes are the result of proposals approved during the SEBI Board meeting held earlier, as released on September 12, 2025, aiming to balance ease of doing business with stricter governance.

The amendments broadly focus on shifting towards a digital approach and refining the rules for related party transactions (“RPT”). This includes mandating electronic payments, removing the need for physical documents, and adjusting approval thresholds to make them more practical for large corporations while ensuring better oversight for subsidiaries.

The amendments are detailed below.

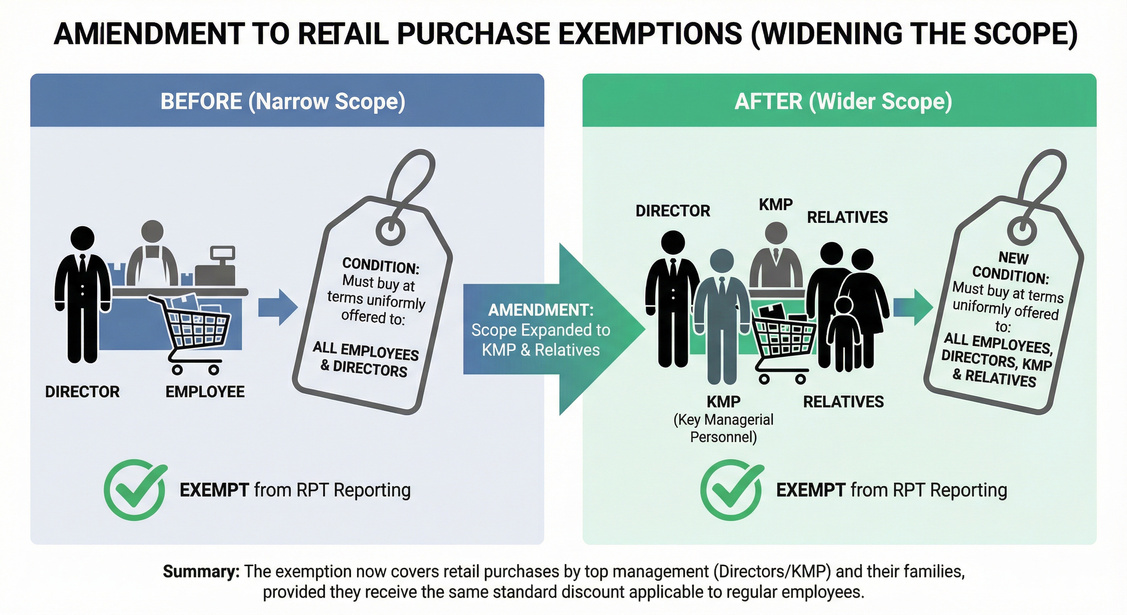

1. Expansion of RPT exemption scope for retail purchases to KMPs and relatives

Existing scenario

Retail purchases of services / resources from a listed entity or its subsidiary by its own directors or employees were earlier not regarded as ‘establishing a business relationship’ and hence were exempted from the definition of ‘RPT’ and compliance requirements as per the SEBI norms (“Existing Exempted Category”). This exemption applied so long as the said purchases were made by the Existing Exempted Category on terms uniformly offered to all employees and directors, ensuring no preferential treatment.

The change

Now, the amendment expands the Existing Exempted Category by (i) adding relatives of directors or key managerial personnels (“KMPs”); and (ii) instead of all employees and directors, only limiting it to KMPs and directors. The condition of uniform-terms is correspondingly expanded so the exemption applies only where the same terms are uniformly available to employees, directors, KMPs and their relatives.

Practical effect

The biggest practical change is that spouses, children and dependent relatives of top management (directors/KMP) can now buy the company’s products / services at the standard ‘employee discount’ rate without the company having to treat every single purchase as a RPT.

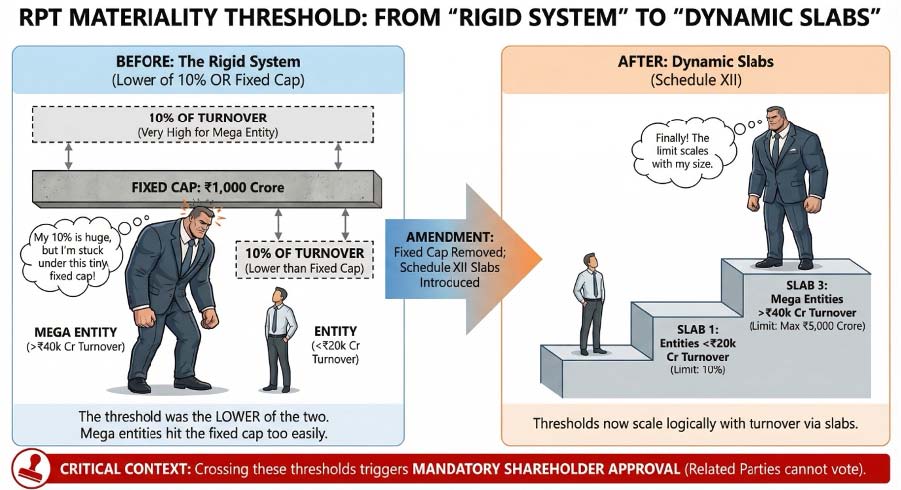

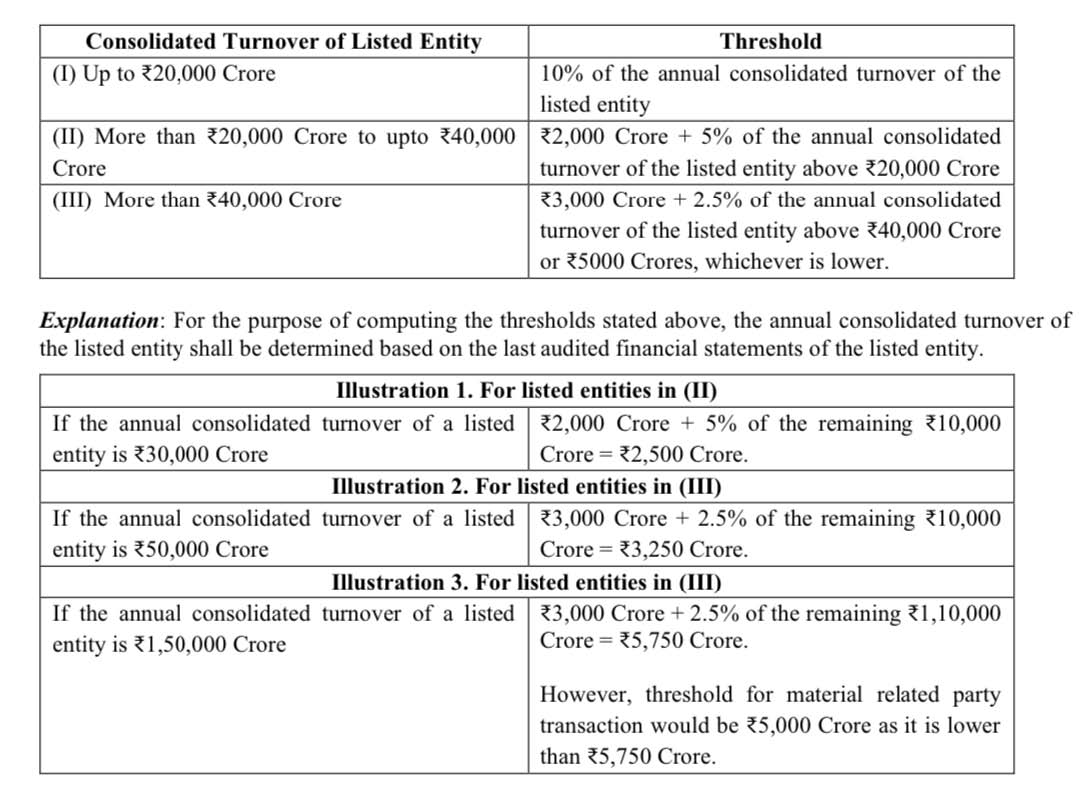

2. Rationalization of materiality thresholds for RPT

Existing scenario

Earlier, the threshold for material RPT, which requires shareholders’ approval was lower of:

- A fixed cap of INR1,000 crore; or

- 10% of the listed entity’s consolidated turnover.

The change

Now, the fixed cap of INR1,000 crore is removed and it is replaced by the new schedule XII slabs as stated below:

Effect

Large corporations no longer hit the uniform cap of fixed INR1,000 crore ceiling. Their threshold now scales logically with their size (up to INR5,000 crore), reducing the need for constant shareholder votes on routine operational matters. For entities with less than INR20,000 crore turnover, the rule effectively remains the same (10% of annual consolidated turnover).

The transaction size of larger companies are usually large which, in the most of the cases, exceeded INR 1,000 crore. Because of the uniform cap of fixed INR1,000 crore, the larger companies were required to obtain shareholders’ approval more often as compared to smaller companies. Hence, the amendment attempts to bring the larger companies and smaller companies at par when it comes

to seeking approval of shareholders for material RPT.

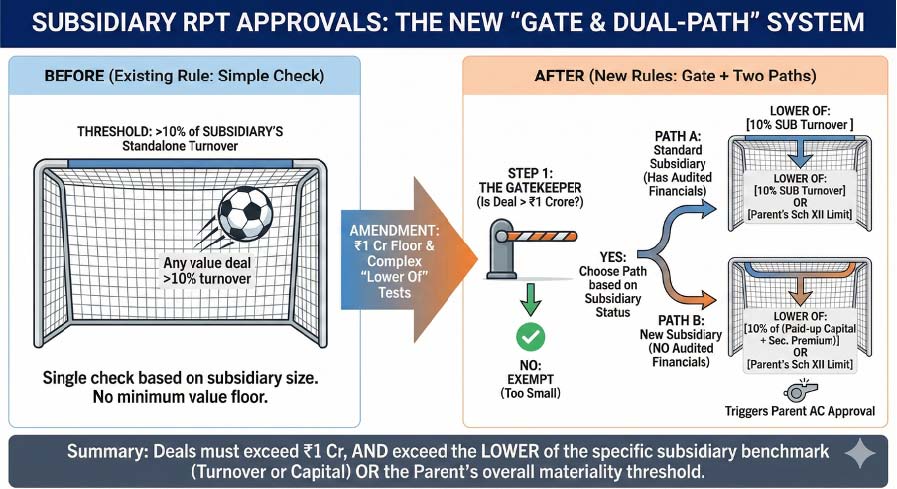

3. Revised approval thresholds for subsidiary RPT

Existing scenario

A RPT where a subsidiary is involved, but the listed parent is not, requires the parent’s audit committee approval if the transaction(s), exceeds 10% of the subsidiary’s annual standalone turnover as per its last audited financial statements.

The change

A new absolute floor is added. Audit committee’s approval is only required for transactions above INR1 crore. If a transaction is below INR1 crore, it doesn’t need approval, even if it exceeds 10% of the subsidiary’s turnover. However, for transactions above INR 1 crore, the threshold is lower of:

- 10% of the subsidiary’s standalone turnover; or

- It’s parent’s new materiality threshold (schedule XII slabs)

Further, if the subsidiary has no audited financial statements of at least one year, approval is required for RPTs exceeding INR1 crore but lower of:

- 10% of the aggregate value of paid-up share capital and securities premium account of the subsidiary; or

- It’s parent’s new materiality threshold (schedule XII slabs)

Effect

The INR1 Crore floor eliminates the compliance burden for trivial transactions in small subsidiaries, allowing the audit committee to focus on meaningful amounts. By introducing the “lower of” test against the parent’s Schedule XII threshold, the amendment ensures that a subsidiary cannot enter into a deal that is considered “material” for its parent company, even if it’s within 10% of that specific subsidiary’s turnover. Further, the amendment for subsidiaries without audited financials plugs a major loophole. Previously, newly incorporated entities had no clear benchmark for approval. Now, their capital base serves as a proxy for size to ensure appropriate oversight from day one.

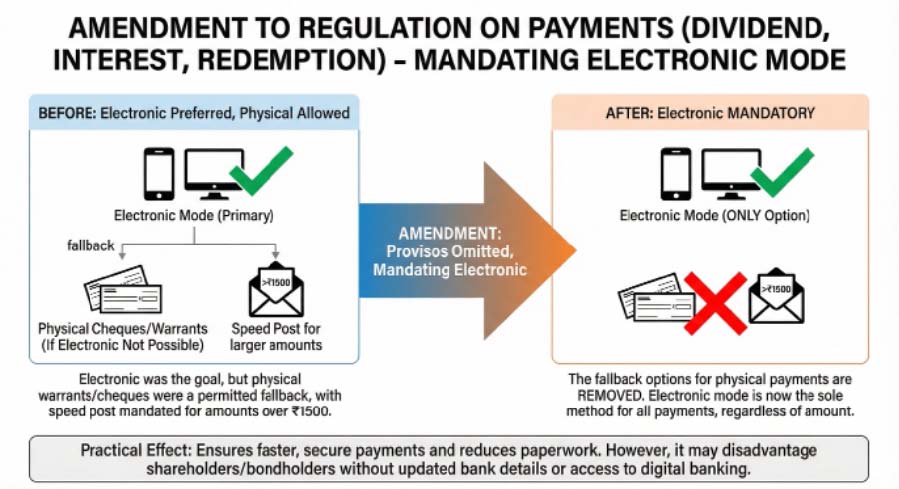

4. Mandatory electronic payment for dividends, interest and redemptions

Existing scenario

Earlier, for payments of dividend, interest or redemption / repayment amounts, electronic payment was preferred, but if it was not possible to pay electronically, companies could issue ‘payable-at-par’ cheques or warrants. For amounts over ₹1500, these had to be sent via speed post.

The change

The amendment removes the option for companies to pay dividends, interest, or redemption / repayment amounts using physical methods like cheques or warrants. Now, the listed entities shall use electronic modes of payment approved by the RBI for all such payments.

Effect

Shareholders who do not have bank accounts updated with the company or depository, or who are not comfortable with digital banking, may face difficulties in receiving their payments. They will now be forced to update their bank details to get their money. However, payment being credited directly to bank account is a much faster way than printing and posting a lot of cheques. Further, it reduces the risk of cheques being lost, stolen, or fraudulently encashed in transit. While reducing paper usage being better for environment, the companies will also save costs on printing and postage.

5. Expanded disclosures and revised submission timelines for annual reports

Existing scenario

Previously, the annual report was required to contain disclosures specifically under the Companies Act, 2013. Regarding submission timelines of annual report, listed entities had to send a copy to the stock exchanges, debenture trustee and their website (by way of publishing) not later than the date of commencement of dispatch to shareholders. If there were any changes to the annual report, the revised version had to be submitted strictly within 48 hours after the annual general meeting.

The change

The amendment broadens the scope in two ways:

- It now includes disclosures required by the statute under which such listed entity is constituted. This is a crucial addition for listed entities that are not standard companies but statutory corporations (like LIC, SBI, etc., formed under their own respective statutes).

- The timeline for submission to stock exchanges, debenture trustee and website now includes a new trigger, i.e., ‘date of submission to the Central or State Government.’ The deadline is now ‘on or before’ dispatch to shareholders OR submission to the government, whichever applies.

Effect

The practical impact is that statutory corporations can no longer claim ambiguity about disclosures as they must explicitly follow their founding statutes for annual reporting. Furthermore, the new timeline closes an information gap, i.e., if a state-owned entity submits its report to the government before sending it to shareholders, it must now simultaneously disclose it to the stock exchange, debenture trustees and its website. This ensures that the government does not get privileged access to the annual report information before the general market.

6. Digital dispatch and timelines for non-convertible securities

Existing scenario

Previously, for holders of non-convertible securities who had not registered their email addresses, the listed entity was required to send a hard copy of a statement containing the salient features of the annual report documents (as specified in Section 136 of the Companies Act). This meant printing and posting abridged versions of the financial statements to potentially a large number of investors. There was also no explicit timeline mentioned in this specific regulation for sending these documents.

The change

The amendment introduces two changes:

- The requirement to send a hard copy of the salient features is deleted. Instead, companies must now send a physical letter containing a web-link (and optionally a QR code) to the full Annual Report on their website.

- A new sub-regulation (1A) specifies that these documents must be sent within the timelines prescribed by the Companies Act, 2013, or the specific statute under which the entity is constituted. If the statute has no timeline, the deadline is the earlier of dispatch to shareholders or submission to the Central/State Government.

Effect

This is a significant move towards digitalization. It drastically reduces the printing and postage costs for companies and has a positive environmental impact by eliminating paper-heavy documents. Investors get direct access to the complete Annual Report via a link/QR code, rather than just an abridged version. Furthermore, the new timeline provision removes ambiguity, ensuring that statutory corporations follow their specific acts, and aligns the disclosure to debt holders with the disclosure to equity shareholders and the government.

Conclusion

In practice, the RPT revisions offer significant breathing room for large corporations, allowing them to execute operational transactions without constant shareholder roadblocks. It signals a mature regulatory approach that prioritizes efficiency and logical thresholds over rigid ‘one size fits all’ mandates. The specific ‘lower of’ tests for subsidiaries allows boards to focus strictly on significant deals and the inclusion of statutory bodies tighten the net where governance risks often hide.

While the shift to digital only dispatch and payments will eventually lower administrative costs and carbon footprints, companies must proactively communicate with investors during this transition to prevent payment failures or information gaps.

Amendments at serial numbers 1, 2, and 3 of this article stated above will come into effect on December 18, 2025, whereas the remaining amendment serial numbers are effective immediately from the notification date, i.e., November 18, 2025.